Technology and Digital have opened up new opportunities for the insurance industry, but also make the future uncertain for large insurance companies. In this article we’re discussing 5 digital trends for insurance, and ask some important maturity measures for those looking to implement a successful digital strategy. The trends we’ll be looking at are:

- Open/API Insurance

- Insurgent Business Models

- Data and Analytics

- Data Privacy and Governance

- Direct Distribution

Insurance Trend 1 – Open Insurance or API Insurance

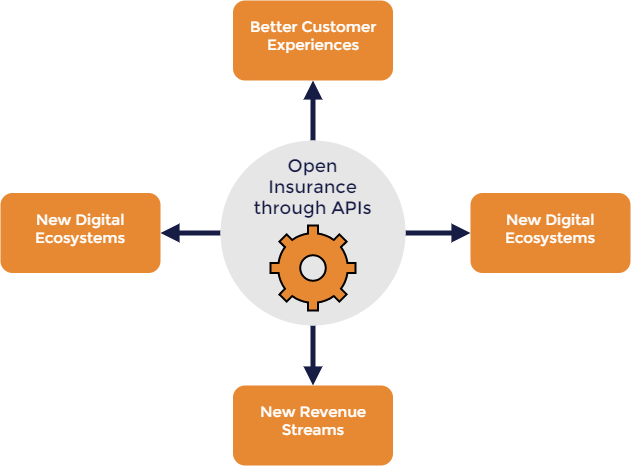

Open Insurance, also known as API Insurance, is a trend gaining traction throughout the industry. Similar to the open banking movement, it involves the move to a connected data ecosystem, powered by open and partnership APIs. Large Insurance companies are looking to establish API platforms and expose their data and products to, and integrating with, third-party providers such as Insurtechs, big tech etc. – providing mutual growth and enabling new business models and revenue streams. A connected open API ecosystem also allows them to integrate data from elsewhere (think Uber using 3rd party Google Maps API as an example) to offer new services.

Open Insurance, also known as API Insurance, is a trend gaining traction throughout the industry. Similar to the open banking movement, it involves the move to a connected data ecosystem, powered by open and partnership APIs. Large Insurance companies are looking to establish API platforms and expose their data and products to, and integrating with, third-party providers such as Insurtechs, big tech etc. – providing mutual growth and enabling new business models and revenue streams. A connected open API ecosystem also allows them to integrate data from elsewhere (think Uber using 3rd party Google Maps API as an example) to offer new services.

One of the open insurance movement’s primary drivers is increasing customer demand for personalized insurance options with more touchpoints. We’re now in an age where consumers expect a frictionless digital experience, with policies tailored to their specific needs instead of a one-size-fits-all approach, and they’re not afraid to take their business elsewhere if companies can’t meet these demands (see later trends for more on new business models and distribution channels).

While the open/API insurance trend is still in its early stages, there are a few examples of successful API ecosystems already established. In 2018 Allianz launched a platform (both open source and enterprise versions) with parts of the Allianz Business System (ABS), to aid with the challenges of digitization and offer a marketplace for sharing services throughout the insurance industry.

And its not just incumbents looking to capitalize on open insurance with API platforms. In 2018 the established Insurtech Lemonade launched its open API, allowing its policies to be sold through any third-party websites or apps.

Maturity Measure: to deliver open/API insurance, are you…

Focusing on building a handful of well-designed and documented public APIs, or focusing on building 1000s of APIs (internal and external) encapsulating your business and IT functions, to be able to fully participate in the open insurance connected ecosystem?

Insurance Trend 2 – Insurgent Business Models

According to Business Insider Intelligence’s recent report, we’re now at a stage of insurance disruption that involves the adaptation of underlying business models. Enabled by a combination of technology and increasing customer demand, some prominent new business models we’re seeing are:

According to Business Insider Intelligence’s recent report, we’re now at a stage of insurance disruption that involves the adaptation of underlying business models. Enabled by a combination of technology and increasing customer demand, some prominent new business models we’re seeing are:

- usage based insurance (UBI) – particularly in the auto insurance sector e.g. pay-per-mile

- peer to peer (P2P) – particularly homeowners and renters insurance

- micro insurance – particularly in the health insurance sector, for external risk e.g. accident, illness, natural disaster

All are aimed at providing consumers with personalized product options, tailored to their needs instead of a one-size-fits-all approach we’ve seen with traditional insurance models.

This trend is now evolving in 2 ways. The first, is incumbent insurers adopting these insurgent business models, e.g. the new Milewise policy from Allstate in the US with a per-mile rate, as well as more traditional telematics-based UBI like AXA’s Flexidrive in Asia with up to 20% discounts for good driving behaviors.

The second evolution of this trend is that Insurtechs are now capitalizing on their insurgent business models by moving from being managing general agents (MGAs) to full-stack insurance companies – to challenge incumbents head on. For example, there are now 5 full-stack Insurtechs in the USA alone – Metromile, Root, Oscar Health, Lemonade, and Next Insurance.

As this trend evolves, we expect to see even further pressure on insurance incumbents to rapidly deliver innovative new products, in support of these insurgent business models, and to meet consumer expectations.

Maturity Measure: to deliver insurgent business models e.g. UBI, P2P, and microinsurance, are you…

Able to expose your existing functionalities as a set of normalized and standardized APIs, approved for reuse as bundle-ready digital building blocks to deliver innovative and personalized products to customers?

Able to support not only current insurgent business models, but poised to be responsive and move fast for whatever comes next?

Insurance Trend 3 – Data and Analytics (IoT etc.)

Connected devices, the Internet of things (IoT), Artificial intelligence (AI), mobile technology etc., are providing insurers with detailed data and analytics which can be leveraged not only to provide better products to customers, but also to reduce operational inefficiencies and associated costs. A few examples of both incumbents and Insurtechs leveraging this trend include:

Connected devices, the Internet of things (IoT), Artificial intelligence (AI), mobile technology etc., are providing insurers with detailed data and analytics which can be leveraged not only to provide better products to customers, but also to reduce operational inefficiencies and associated costs. A few examples of both incumbents and Insurtechs leveraging this trend include:

- the Insurtech Tyche uses an AI-based claim likelihood model as part of the underwriting process, to achieve higher profitability through accurate risk determination

- Nationwide and Toyota Insurance Management Solutions (TIMS) have partnered to launch TIMS BrightDrive, a telematics-based insurance policy with up to 40% discount for customers

- Zurich Spain’s new water-damage prevention technology, Zurich Smart

- John Hancock’s move to “interactive”-only policies where all customers have health data collected through wearables, resulting in discounts and rewards for hitting exercise targets

Robotic process automation (RPA) is another big area for the application of AI and data for insurers. It involves the automation of routine tasks (and at an advanced level combining cognitive capabilities) to drive business results. According to Deloitte, “the IT-enabled RPA market has been growing rapidly at a CAGR of 60.5% from 2014 and is expected to reach US$5 billion by 2020” – so a highly important trend for the industry.

The real success in this trend will be when insurers can leverage data and analytics throughout the value chain, encompassing all the areas we’ve discussed – connected data, analytics and AI, and RPA (or better still R&CA).

Maturity Measure: to deliver results from data and analytics, are you…

Able to facilitate connected data and analytics throughout the insurance value chain, through a set of well-designed APIs exposing your data, and integrating data from elsewhere?

Insurance Trend 4 – Data Privacy and Governance

Regulation around data privacy has been a growing trend across many geographies, at a huge cost to insurers who operate in those regions. Of course, the EU’s General Data Protection Regulation (GDPR) has now been in effect for nearly 2 years, while the California Consumer Privacy Act (CCPA) came into effect in early 2020 (and looks to be setting the pace for other state legislation, with New York looking to be next in line.

Regulation around data privacy has been a growing trend across many geographies, at a huge cost to insurers who operate in those regions. Of course, the EU’s General Data Protection Regulation (GDPR) has now been in effect for nearly 2 years, while the California Consumer Privacy Act (CCPA) came into effect in early 2020 (and looks to be setting the pace for other state legislation, with New York looking to be next in line.

Meanwhile, large insurance companies are moving more data to the cloud as part of IT modernization efforts. These combined factors mean it’s critical for insurers to be able to ensure their data is secure and properly managed (and exposed only to the appropriate consumers) if they are to continually move into the digital economy. Failure to do so can result in hefty fines and reputational damage (for example State Farm’s huge data breach in 2019).

Maturity Measure – to comply with data privacy and governance, are you…

Already undertaking a comprehensive information governance program (for data at rest and in motion)?

Able to report (on an ongoing basis), on the compliance of your data flowing through APIs and Services? Who owns what, where it’s consumed, the flow of data etc.?

Insurance Trend 5 – Insurance Distribution Channels – Direct Distribution

Direct insurance is a distribution trend that’s growing more as insurance becomes more digital. McKinsey reported that direct insurance as a distribution channel has grown across NA, EMEA, and APAC, particularly in Eastern Europe.

Direct insurance is a distribution trend that’s growing more as insurance becomes more digital. McKinsey reported that direct insurance as a distribution channel has grown across NA, EMEA, and APAC, particularly in Eastern Europe.

Meanwhile, PwC says that in a recent survey of US consumers, more than 32% of US respondents – and 50% of those aged 18 to 25 – said they prefer to work directly with insurance carriers. These Gen Zers will be the next generation of insurance customers, so it’s critical for large insurers to be able to support multiple distribution channels, beyond traditional brokers and agency models.

Maturity Measure: to support growing distribution channels e.g. direct, are you…

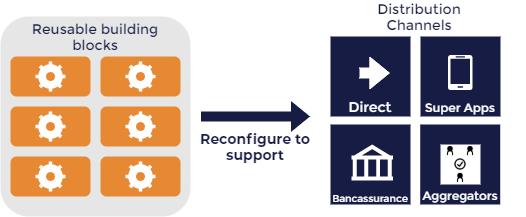

Able to integrate your business and IT capability APIs into alternate distribution channels?

Already supporting direct insurance as a growing distribution channel? If not, how quickly can you respond to this and other growing distribution channels e.g. bancassurance, aggregators, super apps?

While this list of trends is by no means exhaustive, one thing is for certain – large insurers need to become modern digital businesses to excel in this new age of connected data, technology and ever changing trends. But how do they do it? Most are slowed down by tech debt-heavy legacy systems, information silos, and hard-to-find talent (especially when it comes to superstar developers and product managers). Many have already embarked on some level of digital transformation program, often focusing on API First strategies. The key to success is to rapidly mature your API strategy by encapsulating your business and IT functions as a set of abstracted, well-governed, and reusable APIs.

The ignite platform from digitalML helps large insurers transform into digital businesses to become as nimble as digitally native startups, without having to start from scratch.